Introduction

From application to collections, financial institutions rely on specialized platforms to manage every stage of the loan lifecycle. But not all systems are created equal. Understanding where a loan origination system ends and a loan management system begins is critical for lenders navigating complex compliance requirements, borrower expectations, and operational demands.

This guide breaks down the distinct functions of each system, explores when both are necessary, and helps lenders determine the right path forward—whether it’s modular, unified, or end-to-end.

Why the Distinction Matters in 2025

Understanding the difference between loan origination system and loan management system is essential in 2025’s fast-evolving lending environment. As fintech competition intensifies and compliance demands grow, lenders must adopt the right tools at the right stages of the loan lifecycle. Choosing the wrong system can reduce ROI, increase compliance risks, and damage borrower trust.

In the post-pandemic era, digital lending has surged. With this growth comes a need for efficient, integrated platforms that reduce cost, improve borrower experience, and ensure regulatory accuracy. The distinction between origination and management isn’t just semantic; it affects operational efficiency, staffing needs, and customer satisfaction. Knowledge of these systems ensures that lenders can scale operations, maintain compliance, and meet evolving borrower expectations with confidence.

What Is a Loan Origination System (LOS)?

A loan origination system (LOS) supports the front-end of the loan origination process—from application through approval. It covers borrower intake, credit checks, identity verification, and underwriting workflows. These systems are designed to manage the increasing volume and complexity of loan applications while ensuring consistency and compliance.

Modern LOS platforms integrate features like:

- Automated underwriting for faster and more accurate approvals

- Credit decisioning APIs that streamline data pulls from bureaus

- E-signature capture for remote document handling

- KYC/AML compliance modules to mitigate fraud risk

- Rule-based workflows to automate repetitive tasks

With LOS tools, lenders can reduce time-to-fund by up to 35% and boost approval rates by 22%, according to McKinsey & Company. These systems also enhance customer experience by offering intuitive digital applications that reduce friction and improve transparency.

Additionally, loan origination software can include customizable dashboards for loan officers, AI-based fraud detection, and real-time pipeline tracking—ensuring alignment between sales, underwriting, and compliance teams.

What Is a Loan Management System (LMS)?

According to American Banker, a loan management system automates post-origination tasks: servicing, collections, reporting, and customer communication. This spans:

- Payment processing

- Customer account management

- Delinquency tracking

- Built-in audit trails for compliance

- Real-time borrower notifications

A robust loan management system ensures accurate billing, simplifies customer inquiries, and streamlines collections. These systems often support multi-channel communication (email, SMS, portal) and generate compliance-ready reports to satisfy federal and state regulators. A loan servicing system is another core component of an LMS, governing tasks like managing amortization schedules, handling escrow payments, and distributing payoff statements. Effective loan servicing is not only about keeping borrowers current but also about ensuring back-office efficiency and compliance readiness.

An LMS also supports borrower self-service portals, enabling real-time account access and online payments—critical for improving borrower satisfaction. With features like automated payment reminders, dynamic repayment options, and mobile optimization, LMS platforms empower borrowers while minimizing servicing costs. Explore the top 5 essential loan management software features to learn more.

Head-to-Head Comparison: LOS vs LMS

| Feature | Loan Origination System (LOS) | Loan Management System (LMS) |

| Primary Role | Pre-funding (application to approval) | Post-funding (servicing to payoff) |

| Key Modules | Underwriting, KYC, Credit pulls | Payment processing, Reporting, Compliance |

| Owner | Loan Officer, Risk Manager | Servicing Team, Compliance Officer |

| Impact KPI | Approval Rate, Time-to-Fund | NPS Score, Collections Efficiency |

While LOS enhances credit decisioning and onboarding, LMS focuses on long-term borrower relationship and performance monitoring. A key operational insight is that while LOS supports growth by capturing new business, LMS safeguards profitability by ensuring smooth repayment and minimal delinquencies.

These systems also differ in terms of technical integration. LOS platforms prioritize borrower-facing APIs and application flow customization. LMS platforms prioritize ledger accuracy, automated dunning processes, and multi-jurisdictional compliance rules.

Understanding these distinctions is only the beginning. To truly optimize the borrower journey and maximize ROI, many lenders are now asking a more strategic question: when is it time to implement both systems—or consolidate into a single, unified platform?

When Do You Need Both—or an End-to-End Platform?

Most mid-to-large lenders benefit from integrating both systems. Manual handoffs between systems introduce risk, delays, and data discrepancies. Lenders that consolidate multiple tools into a single platform often see significant gains in efficiency and loan volume.

End-to-end lending suites reduce data friction and support a seamless borrower journey. However, best-of-breed systems may allow greater customization. For lenders with complex origination needs but standard servicing processes, modular platforms can offer the best of both worlds. See Vergent’s end-to-end demo.

Cost & ROI Analysis: Separate vs Unified Systems

Standalone LOS or LMS platforms can each cost between $75K and $150K annually in licensing and support. Unified platforms typically cost more upfront, but yield greater savings via:

- Shared data models that reduce redundancy and errors

- Reduced IT maintenance with fewer points of failure

- Lower training costs thanks to unified user interfaces

- Improved compliance tracking with centralized rule management

ROI formula: (Net Benefit − Cost) / Cost

Over five years, unified solutions yield up to 40% higher ROI compared to disparate systems. Hidden costs—like compliance fines from inconsistent data or staffing inefficiencies—further support the case for an integrated approach.

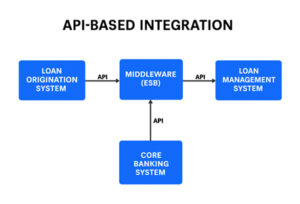

Integration & Data Flow Considerations

Integration is crucial — LOS and LMS must communicate seamlessly to avoid errors and regulatory lapses. This is typically achieved via:

- Real-time open banking APIs that ensure immediate data syncing

- Middleware (ESB) connectors for modular communication

- Data mapping with clear object definitions to maintain integrity

What makes great loan management software? Vergent LMS supports over 80 integrations, enabling fast deployment without custom code. Nightly batch syncs can introduce lag—real-time integration is preferred. Additionally, unified systems reduce the burden of duplicate entry, making it easier to maintain clean and compliant loan files across departments.

Compliance Implications Across the Lifecycle

Regulations apply at every stage. A unified system simplifies audit preparation by keeping all compliance data in one place.

Pre-funding (LOS):

- TILA disclosures

- Reg Z requirements

- Fair-lending reporting

- Adherence to ECOA and HMDA data collection

Post-funding (LMS):

- FDCPA and Reg F for collection practices

- ACH retry limits ()

- State-by-state servicing updates

- UDAAP prevention policies

Unified systems help ensure these requirements are met automatically and are backed by verifiable audit trails. Audit prep becomes easier with standardized reports, version-controlled disclosures, and system-enforced timelines.

FAQs on LOS vs LMS

Q: Can a single platform do both origination and management?

A: Yes. Unified platforms offer both functions to streamline workflows.

Q: How long does migration take if I split systems?

A: A phased migration typically spans 90 days.

Q: What data points must be shared?

A: Borrower info, loan terms, underwriting notes, and payment schedules.

Q: What happens if LOS and LMS aren’t integrated?

A: Data errors, compliance gaps, and poor borrower experience often result.

Q: Who should lead a migration project?

A: Cross-functional teams including IT, compliance, and lending operations ensure success.

Still have questions about where to start or how systems work together in practice? Talk to Vergent about right-sizing your tech stack.

Understanding the Full Lending Lifecycle

The loan origination system is your front line for credit decisioning, while the loan management system is your backbone for servicing. Each system plays a vital role in the lending process. Recognizing the difference between loan origination system and loan management system helps lenders avoid costly overlaps, ensure compliance, and deliver superior borrower experiences.

For end-to-end efficiency, many institutions turn to platforms like Vergent that integrate both LOS and LMS capabilities into a unified solution. These platforms simplify implementation, reduce friction, and provide a scalable infrastructure that grows with your lending goals; even a turnkey lender can benefit from modular or full-suite platforms that allow for rapid deployment while supporting unique compliance, user experience, and integration needs.

Explore best practices for starting a new lending company and other resources from our blog.

Ready to protect your portfolio and your profits?

If you want to learn more about what Vergent’s Loan Management System can do for you, get in touch with us today to schedule a demo and start seeing your KPIs clearer than you ever could.

Explore More from Vergent

- Lending Solutions and Reporting

Learn how Vergent’s reporting & data‑analysis tools help track KPIs and forecast portfolio trends. - AI-Powered Decisioning

Understand how real‑time decisioning and alternative data support smarter KPI monitoring. - Automation and Workflows

See how AI‑powered automation improves efficiency across loan origination to collections.