Automated Payment Matching: The Hidden Cost Saver in Loan Servicing

Introduction

Manual payment processing may seem manageable—until it starts costing you time, money, and borrower trust. In today’s fast-paced lending environment, delays and errors in payment reconciliation can quietly erode your margins.

By the numbers: The ACH Network processed 35.2 billion payments worth $93 trillion in 2025, a 4.9% year-over-year volume increase, according to Nacha. Same Day ACH alone grew 16.7% in volume to 1.4 billion transactions, reflecting borrower demand for instant, efficient payment experiences that lenders must now support.

ACH returns, posting errors, and misapplied payments don’t just create headaches—they increase delinquency risk, inflate staffing needs, and frustrate borrowers. Fortunately, there’s a better way to handle this critical function.

With the right ACH payment software, you can automate the most tedious parts of loan servicing and unlock significant operational savings.

The Problem with Traditional Payment Processing

Many lenders still rely on a patchwork of spreadsheets, outdated tools, and manual workflows to manage borrower payments. This creates bottlenecks, introduces human error, and slows down every step of the servicing process.

Common challenges include:

- Manual matching of ACH, debit, and check payments

- ACH returns not flagged in real time

- Poor payment visibility for borrowers

- Separate vendors creating data silos and higher fees

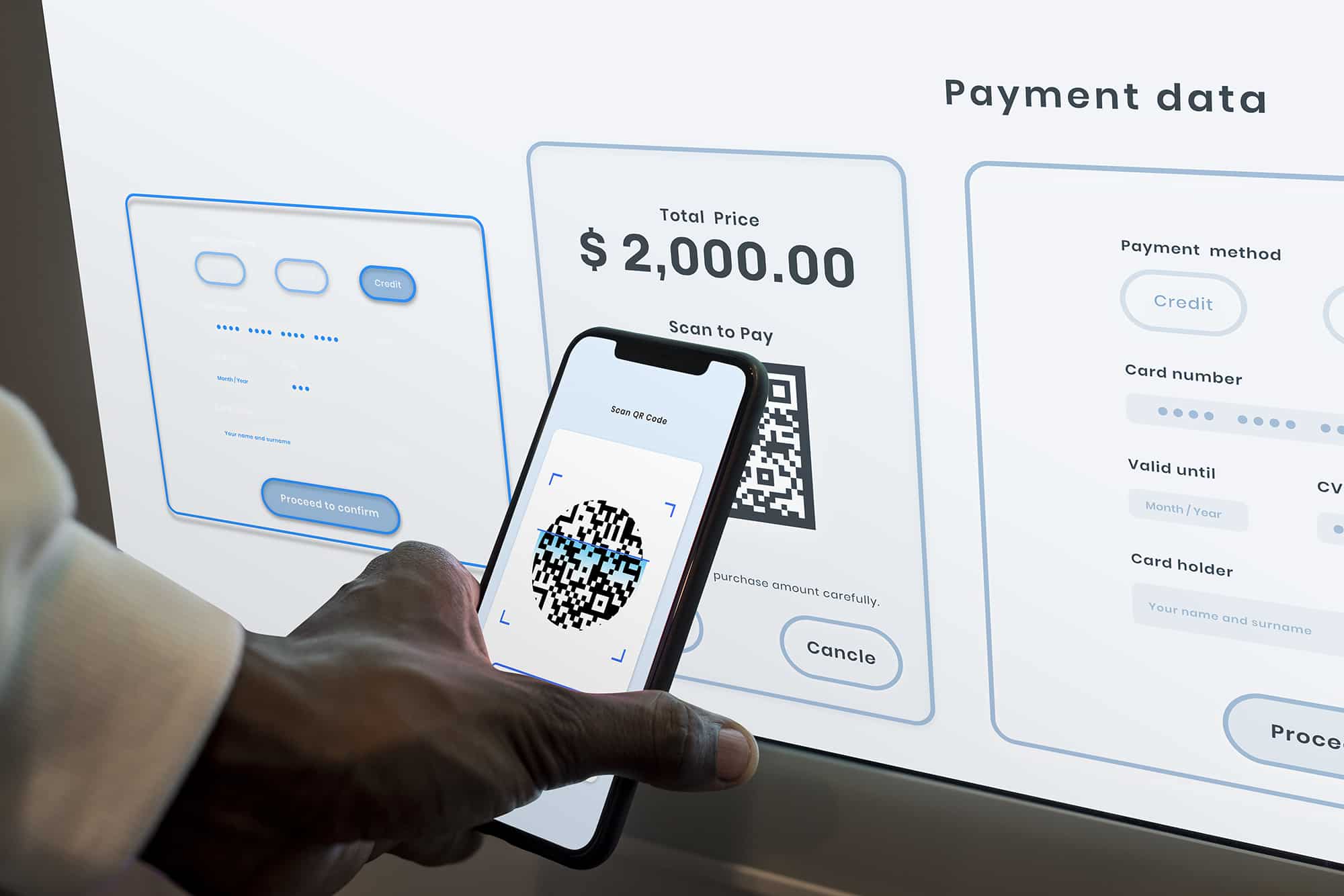

What Is Omnia Pay?

Omnia Pay is an embedded ACH payment software platform built directly into Vergent LMS. It automates reconciliation, improves borrower experience, and eliminates the need for third-party middleware or manual tracking.

Key features of Omnia Pay include:

- Accepts ACH, debit card, and credit card payments

- Automatically matches payments to borrower accounts

- Instantly flags ACH returns and NSFs

- Enables one-click payments via web, app, or SMS

- Syncs with collections and accounting in real time

Real-World ROI: One Client’s Results

Lenders who adopt Omnia Pay often see immediate operational improvements. One client reduced their NSF follow-ups by 40% after deployment. They also saved 2 full-time employee hours per day through automatic reconciliation and achieved a 20% faster daily close process.

Additional benefits included:

- Fewer posting errors

- Reduced reliance on call center support

- Elimination of manual double entry

Developer Friendly, Auditor Approved

Omnia Pay is built for security, compliance, and long-term scalability. Whether you’re preparing for an audit or expanding your loan volume, you can trust the system to handle it all.

- PCI-DSS compliant for payment security

- Role-based access controls

- Real-time audit logs of every transaction

- Instant reporting for finance and compliance teams

Conclusion: Eliminate the Hidden Costs of Manual Servicing

You wouldn’t tolerate manual underwriting in 2025—so why accept manual payments? ACH payment software like Omnia Pay removes the friction and inefficiencies that drag down servicing operations.

Whether you’re scaling a new lending program or upgrading your tech stack, Omnia Pay helps you cut costs, reduce risk, and accelerate collections—all without the overhead of traditional payment tools.

Get Started Today!

Want to process your first $25,000 in payments with no fees? Start your free Omnia Pay trial today.

What Is ACH Payment Processing in Loan Servicing?

ACH (Automated Clearing House) payment processing in loan servicing is the electronic transfer of borrower payments directly from their bank account to the lender’s account on scheduled due dates, processed through the Federal Reserve’s ACH network. Modern loan management systems initiate ACH debits automatically based on payment schedules, post the received funds to the correct loan account in real time, and handle payment failures with automated retry logic and delinquency notifications. ACH automation eliminates manual payment collection, reduces failed payment rates, and provides same-day or next-day payment settlement.

ACH Payment Processing Feature Checklist

- Automated debit initiation, System submits ACH debit files to the Federal Reserve automatically on due dates, without manual intervention

- Same-day ACH support, Ability to process same-day ACH for missed or urgent payments (available on all ACH payments since 2018)

- Return code handling, Automatic processing of NACHA return codes (R01 insufficient funds, R02 account closed, etc.) with appropriate retry or delinquency trigger logic

- Payment matching, Automatic matching of received payments to correct loan accounts without manual reconciliation

- Regulation E compliance, Automated ACH authorization management, including pre-notification requirements and revocation handling

- Multiple payment channels, Support for ACH alongside card, phone, and online portal payments, all posting to the same loan ledger

- Real-time ledger posting, Payments reflected in borrower balance and lender portfolio data immediately upon settlement

Frequently Asked Questions

What is automated payment processing in loan servicing?

Automated payment processing in loan servicing refers to the system-initiated collection, posting, and reconciliation of loan payments, typically via ACH bank debit, without manual staff involvement. On a scheduled payment date, the LMS automatically generates and submits an ACH debit request, receives the settlement confirmation, applies the payment to the correct principal and interest components of the loan, updates the borrower’s balance, and posts the receipt to the lender’s ledger. Failed payments trigger automated retry logic and delinquency workflows. The entire process operates without any payment processing staff involvement for standard payments.

How does ACH payment automation reduce loan servicing costs?

ACH payment automation reduces servicing costs in four ways: (1) eliminates the staff time required to manually process, post, and reconcile payments, particularly impactful at high loan volumes, (2) reduces payment failure rates through optimized retry logic and borrower reminder notifications before due dates, (3) eliminates paper check processing costs (postage, handling, deposit, clearing time), and (4) reduces inbound payment inquiry calls because borrowers can view their payment history in a self-service portal rather than calling. Lenders report 60-80% reductions in payment-related staff hours after implementing full ACH automation.

What happens when an ACH payment fails?

When an ACH payment fails, the Federal Reserve returns the transaction with a NACHA return code indicating the reason (R01, insufficient funds, R02, account closed, R03, account not found, R07, authorization revoked, etc.). A modern LMS handles each return code appropriately: insufficient funds returns trigger an automated retry (typically 1-3 attempts on subsequent business days); account closed or not found returns trigger a delinquency workflow and borrower notification to update payment information; authorization revoked returns halt ACH processing and require manual borrower re-authorization. Failed payment handling logic should be a key evaluation criterion in any LMS selection.

Does Vergent LMS support ACH payment processing?

Yes. Vergent LMS includes automated ACH payment processing as a core capability. The platform initiates ACH debits automatically based on payment schedules, handles all return code types with configurable retry and delinquency logic, posts payments to the correct loan accounts in real time, and maintains a complete payment history audit log. Vergent integrates with leading ACH processors and bank connectivity solutions through its 80+ pre-built integration ecosystem, giving lenders flexibility in their ACH processing provider while maintaining unified payment management within the Vergent platform.

Related Reading

- What Makes Great Loan Management Software?, The 12-feature checklist every lender should use to evaluate platforms.

- What Is an API in Lending?, How open APIs power modern lending integrations and automation.

- What Is a Loan Management System?, Full guide to LMS features, benefits, and what to look for.