How Automated Borrower Communications Reduce Defaults and Cut Servicing Costs

How Automated Borrower Communications Reduce Defaults and Cut Servicing Costs

Most loan defaults don’t begin with a borrower who decides not to pay. They begin with a borrower who got busy, forgot, assumed the payment would sort itself out, or simply didn’t know what to do when they fell behind. The research on this is consistent: consumer surveys by the CFPB find that the majority of consumers with past-due accounts report lacking information about their options, not an intentional decision to default.

That is a solvable problem. The lenders who are outperforming on collections and borrower retention in the current environment are doing so by communicating more effectively, not by adding collectors. They are using automated, triggered messaging that reaches borrowers on the channel they actually monitor, at the moment when the message is most relevant, with content that is specific to their account.

This post covers how automated borrower communication works in a modern loan management platform, which scenarios it covers, and what it delivers in practice.

Why Email Alone Is No Longer Sufficient

For more than a decade, email was the default channel for lender-to-borrower communication. It was inexpensive, easy to automate, and auditable. It remains useful for document delivery, statement notifications, and compliance disclosures, but as a primary channel for time-sensitive payment communications, its effectiveness has declined.

Email open rates in financial services hover around 20 to 25 percent, according to benchmarking data from Mailchimp and the Direct Marketing Association. For a payment reminder that needs to land before a due date, a 20% open rate means four out of five borrowers don’t see it.

SMS performs differently. CTIA’s wireless industry survey data consistently shows that text messages have open rates exceeding 95%, with the majority read within three minutes of receipt. For a payment reminder or an NSF notification, that immediacy is operationally significant.

A modern borrower communication strategy uses both channels, SMS for high-urgency, time-sensitive messages; email for documentation-heavy or compliance-required communications, with the channel selection driven by message type and borrower preference.

The Five Communication Scenarios That Drive the Most Value

Not all automated communications are created equal. The highest-value automated messages are those tied to specific, time-sensitive account events where borrower awareness directly influences financial outcomes.

1. Pre-Due-Date Payment Reminders

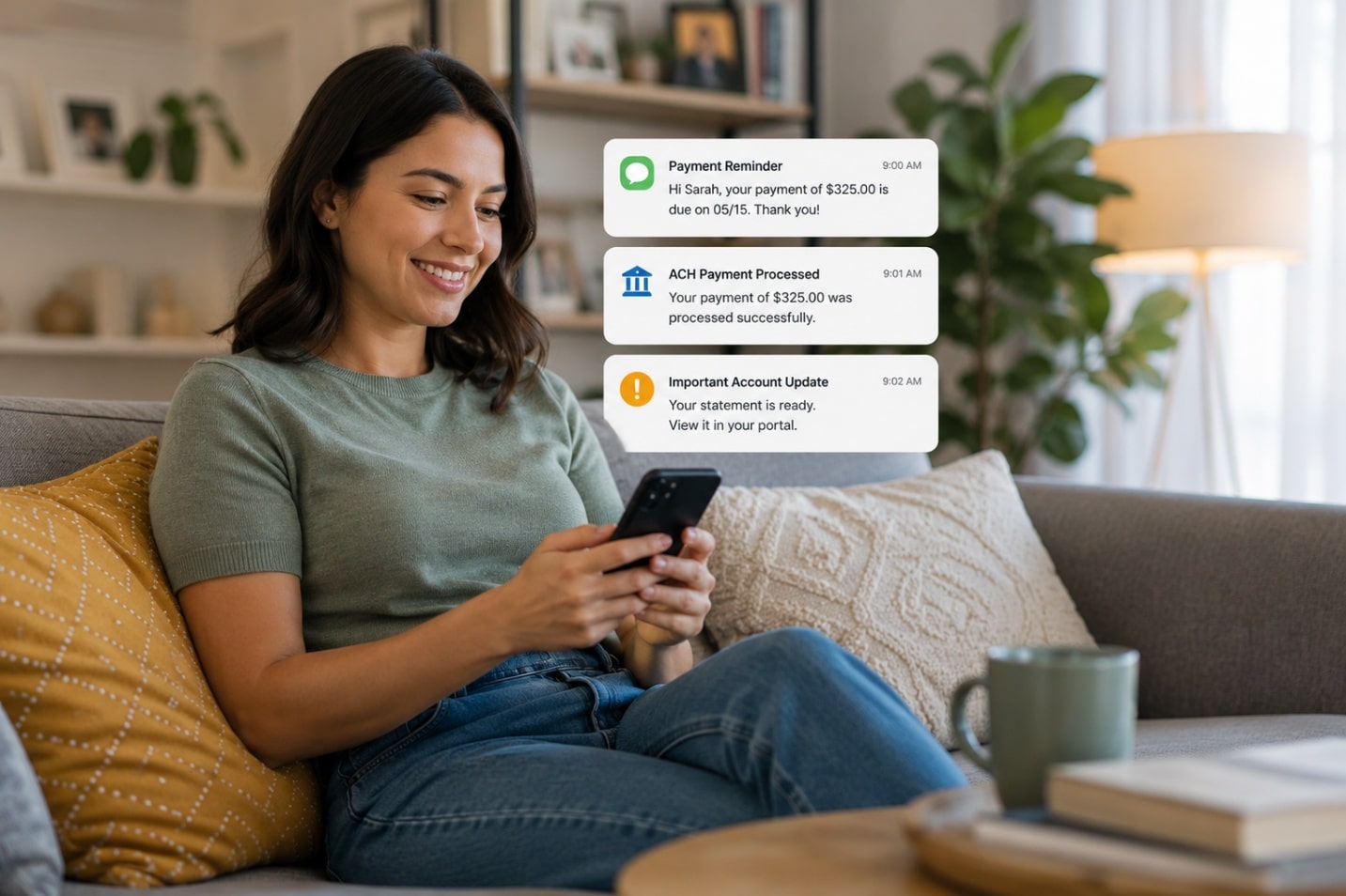

A payment reminder sent 3 to 5 days before a due date, particularly one that acknowledges the borrower’s auto-pay status, is the single highest-impact proactive communication a lender can send. For auto-enrolled customers, the message confirms that the payment is coming and prompts them to ensure funds are available. For non-enrolled customers, it creates an opportunity to initiate payment before the due date.

Vergent’s Communication Manager allows separate reminder templates for auto-enrolled and non-enrolled borrowers, with configurable send timing and account-specific detail, such as the exact payment amount, due date, and current balance, pulled dynamically from the loan record.

2. ACH Return Notifications

When an automatic payment returns, for insufficient funds, a closed account, or other reason, the borrower often doesn’t know immediately. The first notice many borrowers receive under manual processes is a late notice that arrives days later, by which point the account has already moved to past-due status and a collections interaction is required.

An automated return notification sent within hours of the return posting gives the borrower the earliest possible opportunity to resolve the situation, call to reschedule a payment, provide new banking information, or make a payment by an alternative method. The earlier the borrower is aware, the earlier the resolution.

3. Tiered Past-Due Messaging

A borrower who is 4 days past due should not receive the same message as a borrower who is 28 days past due. The tone, the urgency, the content, and the available options are all different. Tiered past-due communication sequences allow lenders to configure progressive messaging that escalates appropriately as accounts age.

A typical tier structure:

- Days 1–7: Soft reminder, assumed oversight, easy path to payment

- Days 8–15: More direct, payment options emphasized, specific balance provided

- Days 16–30: Urgency tone, consequences of continued non-payment addressed

- 31+ days: Collections engagement, hardship program options introduced

Each tier fires automatically based on the account’s days-past-due status, without a collector manually initiating each message.

4. Statement Availability Notifications

For line of credit products and any product that generates periodic statements, a notification that directs borrowers to log in and review their statement, with a direct link to the customer portal, reduces inbound inquiries about balances, due amounts, and payment history. Borrowers who regularly access their portal are more engaged with their account, and engaged borrowers default at lower rates.

5. Post-Payment Confirmations

A payment confirmation message sent after a successful payment posts serves two purposes: it reassures the borrower that the payment was received (reducing “did my payment go through?” calls), and it reinforces positive payment behavior with immediate acknowledgment.

Two-Way SMS: When Borrowers Need to Respond

Automated outbound messaging addresses a significant portion of borrower communication volume. But there are interactions that require a borrower response, payment arrangement requests, updated banking information, questions about payoff amounts, that a one-way message cannot resolve.

Two-way SMS capability, through Vergent’s integration with OmniaText, allows borrowers to reply directly to automated messages and initiate conversations with servicing agents. The platform supports real-time, bidirectional SMS threads logged directly on the customer profile, giving agents visibility into the full conversation history alongside the account record.

OmniaText supports custom workflow triggers, so borrower responses can initiate automated actions, routing a reply indicating hardship to a collections agent queue, for example, or triggering a link to a payment portal when a borrower asks how to pay. Compliance features include STOP/STOPALL handling, TCPA-aligned consent workflows, and SOC-certified message logging.

Research from CTIA shows that Americans exchange billions of text messages daily, with SMS remaining the most universally accessible mobile communication format across age groups, income levels, and device types. For consumer lenders serving broad demographic profiles, SMS is the most inclusive channel available.

Configurable Templates: Compliance Without the Bottleneck

Every consumer lending communication carries regulatory exposure. The FDCPA governs collections-related communications. The TCPA governs automated text messages. State consumer protection statutes add jurisdiction-specific requirements in many states. Maintaining compliance in a high-volume automated communication environment requires templates that are reviewed, approved, and consistently applied, not messages drafted on the fly by individual agents.

Vergent’s Communication Manager uses configurable templates with dynamic field insertion, pulling account-specific data (name, balance, due date, payment amount, payoff amount) into pre-approved message structures. When regulations change, the template is updated once and the change applies to all future sends automatically.

The CFPB’s UDAP examination framework evaluates whether borrower communications are accurate, not misleading, and not unfair. Template-based automated communications, reviewed and approved by compliance staff before deployment, are inherently more defensible than agent-initiated ad hoc messaging.

Self-Service as a Communication Strategy

The highest-efficiency communication outcome is one where the borrower resolves their own question without a live interaction at all. Vergent’s customer self-service portal gives borrowers 24/7 access to:

- Current account balance and available credit (for LOC products)

- Payment due dates and upcoming payment schedule

- Payment history

- Statements (downloadable)

- Loan documents

- The ability to make one-time payments directly

Automated message content is designed to direct borrowers to the portal for self-service actions, “Log in to view your statement” rather than “Call us for your balance.” This reduces inbound call volume while improving the borrower’s access to their own information.

For line of credit customers, the portal also enables draw requests, the borrower can initiate an advance directly from the portal without a staff interaction, subject to configured rules (available credit, account standing).

What Lenders Are Reporting

Lenders using a combination of pre-due-date SMS reminders, auto-pay enrollment, and tiered past-due messaging consistently report meaningful reductions in early-stage delinquency, accounts that might have gone 7 to 15 days past due clearing in the 1 to 5 day bucket instead, because the borrower was reminded before the due date and addressed the situation promptly.

The channel shift also affects agent productivity. When automated communications handle a significant share of routine borrower outreach, collectors can concentrate their time on accounts that require genuine negotiation and judgment, later-stage delinquency, hardship situations, disputes. This is not a reduction in staffing; it is a reallocation of staff capacity to higher-value work.

Frequently Asked Questions

What is automated loan communication software?

Automated loan communication software sends pre-configured messages to borrowers at specific times based on account events, payment due dates, return occurrences, statement generation, past-due status, without requiring staff to initiate each message. Messages are sent via SMS, email, or both, with content pulled dynamically from the loan record.

How do payment reminders reduce loan default rates?

Payment reminders reduce defaults by ensuring borrowers are aware of upcoming due dates before they miss them. For auto-enrolled customers, reminders prompt fund availability verification. For non-enrolled customers, reminders create an opportunity to pay proactively. Studies across consumer lending segments consistently show lower early-stage delinquency rates for portfolios with active pre-due-date communication programs.

What is TCPA compliance in SMS lending communications?

The Telephone Consumer Protection Act (TCPA) requires prior express written consent for automated text messages sent for marketing or informational purposes, including collections-related SMS. A compliant lending SMS platform must document consent at origination, honor opt-out requests (STOP/STOPALL) promptly, and maintain records of consent and opt-out history. OmniaText, integrated with Vergent LMS, includes built-in TCPA compliance handling.

Can SMS payment reminders integrate with loan management software?

Yes. When the communication platform is integrated with the LMS, as OmniaText is with Vergent, messages can include dynamic account data (specific balance, due date, payoff amount) pulled directly from the loan record. This enables personalized, accurate messages without manual data entry.

What is two-way SMS in loan servicing?

Two-way SMS allows borrowers to reply to automated messages, ask questions, and initiate conversations with servicing agents via text. Replies are logged on the customer profile alongside the account record, giving agents full visibility into message history. Two-way capability converts SMS from a one-way notification channel into a full communication channel.

How does self-service borrower portal reduce servicing costs?

A self-service portal reduces inbound call volume by giving borrowers 24/7 access to balance information, payment history, statements, and online payment capability. When automated communications direct borrowers to the portal for self-service actions, a significant share of routine inquiries is resolved without staff involvement, reducing per-loan servicing cost and freeing agent time for higher-value interactions.

Summary

The gap between lenders who perform well on delinquency and those who struggle is often not credit quality, it is communication quality. Borrowers who are kept informed, who receive reminders before due dates, who understand their options when they fall behind, and who have easy access to their own account data are less likely to default and more likely to resolve past-due situations quickly.

Automated, triggered, multi-channel communication, deployed through a properly configured loan management platform, delivers that outcome at a fraction of the cost of manual outreach.

Vergent LMS and OmniaText work together to give lenders a complete, compliant borrower communication infrastructure. Schedule a demo to see how the system configures to your loan products and communication strategy.

Sources: CFPB Consumer Experiences with Debt Collection | CTIA Annual Wireless Industry Survey | Mailchimp Email Marketing Benchmarks | CFPB UDAP Examination Framework | NACHA ACH Operating Rules

If you’re looking to automate borrower communications at scale, Vergent’s loan servicing software has built-in SMS, email, and payment automation tools built for lenders.